- How to know when you’re ready to open a new account

- The advantages of various accounts and how they fit into your life

- How to maximize your savings and returns with each account

Lesson How to know when you're ready to open another account

Which accounts are right for me?

Learn about choosing the right accounts for your portfolio

When it comes to saving and investing, there are lots of different account options available to you. While TFSAs (tax-free savings account) and RRSPs (registered retirement savings plan) are two popular choices, there are others that could also benefit you and suit your needs.

Since TFSAs and RRSPs have annual contribution limits, you may find yourself exploring other options when you hit your yearly threshold with these accounts. If you’re in a financial position to save more, it could be the perfect time to open a new account.

What kind of account should you open? That depends on your needs, goals, and home life (whether you’re married, have children, etc). With that, let’s delve into some valuable choices so you can weigh your options thoroughly.

Saving for your first home? Take the first step with an FHSA.

A First Home Savings Account (FHSA) is a tax-free account for first-time home buyers that combines many of the benefits found in TFSAs and RRSPs:

- Contributions are tax-deductible: just like with an RRSP, contributions to an FHSA can be claimed as a deduction on your taxes

- Qualifying withdrawals are tax-free: similar to a TFSA, withdrawals are not added to your taxable income, so long as they are withdrawn to pay for a qualifying home, among other conditions

- You have $8,000 of contribution room every year, plus up to $8,000 of unused carry forward from the prior year, up to a lifetime maximum of $40,000

Learn more about the FHSA’s benefits, how it works, and if you qualify as a first-time home buyer here.

Have kids? Get their tuition savings started with an RESP.

If you have children and one of your goals is to help send them to college or university, a Registered Education Savings Plan (RESP) could be a great asset. RESPs are tax-sheltered, which means that any investments in the account, such as stocks and ETFs, can grow tax-free. You won’t receive any tax deductions for contributing to an RESP, but (and this is a big but) the Canadian government provides grants based on how much you contribute.

By tucking away money for your child’s post-secondary education, the government helps pitch in through two types of federal grants: the basic Canadian Education Savings Grant (CESG) and additional CESG.

- Basic CESG: is a grant of 20% of contributions made to a beneficiary until the year they turn 17. The yearly grant limit is $500. To maximize the yearly grant, parents need to contribute $2,500 [$2,500 (contribution amount) x 20% (matching rate) = $500, yearly maximum]

- Additional CESG: is an additional grant from the government to help save for your child's education. This grant is based on the net family income of the child's primary caregiver (the individual who receives the Canada Child Tax Benefit)

The government allows for a lifetime maximum contribution of up to $50,000 and up to $7,200 in basic CESG grants per beneficiary (child).

The sooner you open an RESP for your child, the more time you have to save and the more time it has to grow from factors like compounding. This helps remove the strain of sudden, large tuition fees when the time comes around, and provides a helping hand from the government in paying for it. You can learn more about RESPs here.

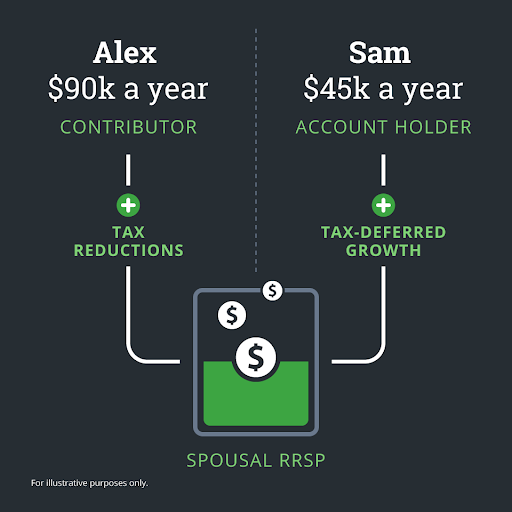

Married or common-law partners? A Spousal RRSP could benefit you both.

When you think about retirement, does that include living comfortably with a special someone? While an RRSP is a great start if you’ve begun thinking about retirement, a spousal RRSP lets you work towards your goals together.

Spousal RRSPs are ideal for couples who want to invest in a nest egg together and have a considerable gap between their incomes. Plus, spousal RRSPs are ripe with tax-related benefits for both partners. Contributions to the account are tax-deductible, which is beneficial for the higher-earning spouse. Meanwhile, the lower-income spouse can reap tax-deferred growth from the spousal RRSP’s investments.

When opening a spousal RRSP you need to set a contributor and the account holder. Also known as an annuitant, the account holder (typically the lower-income partner) owns the RRSP and will ultimately be withdrawing from it. Meanwhile, the contributor (typically the higher-income partner) can make tax-deductible contributions to the account.

Let’s look at an example to see how it works. Alex and Sam open a spousal RRSP together, and they name Alex as the contributor because she has a higher salary. Since Alex will be in a higher tax bracket, her contributions to the spousal RRSP will provide valuable deductions on her income taxes. Meanwhile, Sam can reap tax-deferred growth from the spousal RRSP’s investments, which could include stocks, ETFs, or other products available through a standard RRSP.

It’s important to note that, when it comes to Spousal RRSPs, your yearly RRSP contribution limit still applies. For example, if your annual contribution limit is $10,000 and you put $5,000 into a spousal RRSP (as the spousal RRSP’s contributor), you’d have $5,000 left in contribution room for your personal RRSP. However, your spouse’s limit is not impacted by your contributions to the spousal RRSP. You can learn more about Spousal RRSPs here.

Just looking to invest some extra cash? Consider a Margin or Cash account.

Whether you’re single, married, or anywhere in between, a Margin or Cash account is a great avenue if you want to invest extra funds. If you’ve maxed out your RRSP and TFSA contributions for the year, these accounts provide you with access to investment options like stocks, ETFs and more, giving your savings the chance to grow on their own.

If you’re interested in trading on your own and hand picking your stocks, a Self-Directed Margin account could be a great fit. You can create your own portfolio with no contribution limits, so you can invest as much as you want. Margin accounts also allow you to borrow money to invest. On top of all that, Canada’s Capital Gains Tax means only half (50%) of your first $250,000 in an individual account and two-thirds (66.67%) of other capital gains (like in business or trust accounts, or beyond the first $250,000 in individual accounts) will be taxed.

If you like the sound of a Margin account but would prefer someone do the investing for you, that’s where a Questwealth Portfolios Cash account comes into play. Questwealth Cash accounts work the same way as Margin accounts, except your portfolio is built for you and you can’t borrow money for your investments. That being said, the sooner you get started - whether that’s through Margin, Cash or any other account - the more time your account will have to benefit from compounding.

You can learn more about Margin accounts here, and Questwealth Cash accounts here.

How do I get started?

Whichever account you choose, Questrade is here to support you along the way. You can open an account entirely online, and it only takes a few minutes to get started. Whenever you’re ready to jump in, we’re happy to help.

Open an accountNote: The information in this blog is for educational purposes only and should not be used or construed as financial or investment advice by any individual. Information obtained from third parties is believed to be reliable, but no representations or warranty, expressed or implied, is made by Questrade, Inc., its affiliates or any other person to its accuracy.

Related lessons

Want to dive deeper?

Locked-in accounts

Explore how you can use locked-in accounts such as LIRA, L-RSP, pension transfers, and what you can invest in them.

View lessonRead next

Choosing the right products for your portfolio

Discover the different investment products offered at Questrade.

View lessonExplore

Questrade trading platforms

Discover all of Questrade’s trading platforms and decide which one is best suited for you, and your investment style.

View lesson