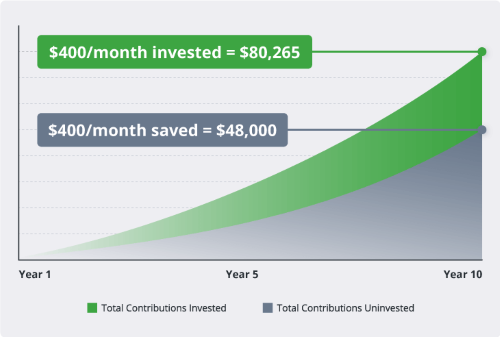

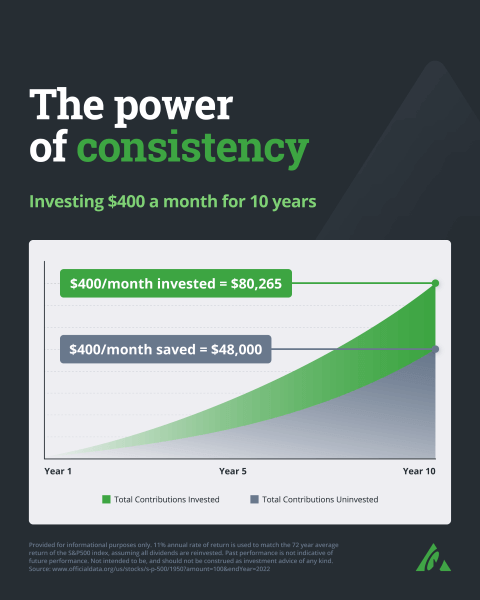

Have you ever confused saving with investing? This is an understandable mistake, as they are often used interchangeably in casual conversation. Both saving and investing involve setting aside money for the future, just in different ways. However, it’s important to understand the differences between the two to make informed financial decisions, set goals, and manage risk effectively.